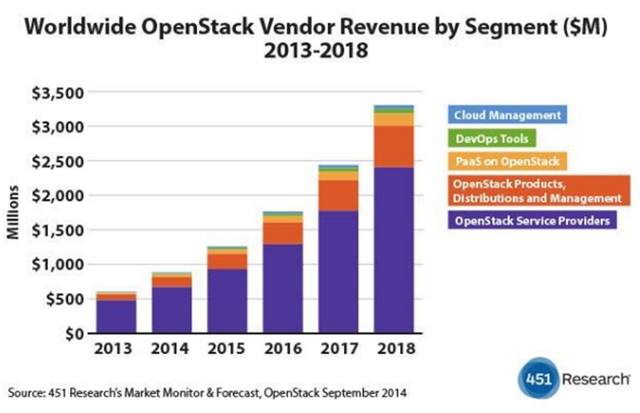

OpenStack began as computing project between Rackspace and NASA and was eventually open sourced. This resulted in a fevered frenzy about how the project would become the de-facto cloud platform used by developers and solution engineering companies worldwide. A year ago, RedHat which incidentally is one of their largest supporters, went on to claim that:

Since 2011, when OpenStack was first released to the community, the following and momentum behind it has been amazing. In fact, it quickly became one of the fastest growing open source projects in the history of open source. Now, with nearly 700 community sponsors, over 600 different modules, and over 50,000 lines of code contributed, OpenStack has become the default platform of choice for much of the private and public cloud infrastructure.

The above quote was from

That claim was of course utter hogwash as we in the industry are prone to do, more so if we are stuck in marketing or sales. In order to put that into perspective a quick peek at the cloud market sets the grand stage:

Cloud computing is projected to increase from $67B in 2015 to $162B in 2020 attaining a compound annual growth rate (CAGR) of 19%. Gartner predicts the worldwide public cloud services market will grow 18% in 2017 to $246.8B, up from $209.2B in 2016.

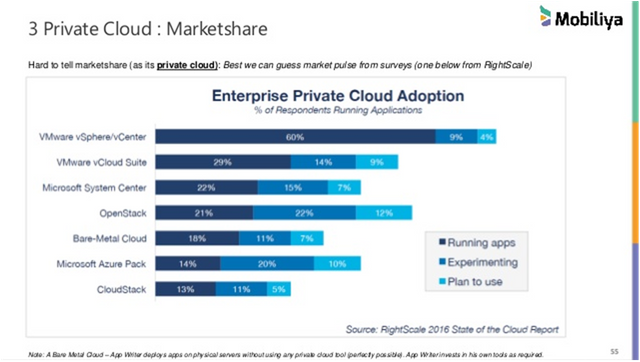

So while the public cloud space is upwards of $200 Billion the OpenStack market share is around 1.5% of that number. IBM which uses a version of OpenStack called BlueBox owns almost 15% of the global cloud services market but much of that cannot be attributed to OpenStack the technology. It is more about the leverage that IBM has over its customer base. In addition private cloud “guesstimates” have OpenStack taking a 20% cut of the overall market share.

There are large companies like American Airlines or JP Morgan that have very strong IT teams and use OpenStack for niche production use cases. It is also being deployed over public clouds like AWS and Azure.

However stories of deployment failures are rising and the success rate is below 50% for most adopters. The euphoria is over and companies have started cutting back on their involvement with OpenStack.

Intel Quit and so did Mirantis which was earlier a pure play OpenStack solution provider.

An obvious threat is application specific container infrastructures like Kubernetes which is eating up private cloud deployments posing a real threat to pure play cloud deployment stacks.

Most experienced industry observers will intuitively know that losing partner momentum is a dangerous thing in such fast paced environments. There is no catching Amazon or even stragglers like Google, Microsoft or IBM.

Where does OpenStack go from here?

Never fear Edge Computing is here

Edge Computing is emerging as last mile cloud connects and addresses a legitimate shortcoming of cloud infrastructures. Public clouds are already heavy with tremendous influx of data and steady rise in computing sprawl.

But an explosion of data will occur with the emergence of IoT, autonomous automobiles, home automation, Industry 4.0 initiatives, remote manufacturing, etc. This data and associated decision making elements cannot be outsourced into the cloud. Real life latencies are so minute that a cloud will just not cut it. E.g. Imagine a hospital that is running life saving equipment cluster connected to an AI decision support system. It cannot hope to save a patient’s life by pushing this into the cloud.

The solution is to delegate cloud functions to the very edge next to the application. In other words, the application (compute+storage+network) either runs on site or at a last mile Telco exchange but still possesses a link-up to the cloud.

The world edge computing market will grow by a compound annual growth rate of more than 30% from 2018 to 2022, Taipei-based market research firm TrendForce forecasts. The market should be worth $3.24 billion by 2025, Grand View Research found in March.

A report by Transparency Market Research (TMR) estimates the global edge computing market will reach USD 13 Billion by 2022.

Here are some possible locations for edge computing workloads: an autonomous car, home automation rack, mobile ICU stretcher, manufacturing floor, conveyer belt system at the airport, AI anti burglary system in a jewellery shop, etc.

As we shall see, Edge Computing and OpenStack have a very strong reason to support each other

Let us classify Edge Computing

We will categorize based on criticality of the use case:

- Real Time Decision Making: These are applications that cannot tolerate any disruption and survive on very low latencies. E.g. autonomous cars

- Caching or Store-Forward Engines: These are typical data collection clusters where the edge application will interface with its users, buffer the information and then push it through in some kind of altered form to the core. E.g. weather monitoring hub

- Non Real Time Decision Engines: Applications that can tolerate higher latencies but will not have the bandwidth to constantly stream data to the core. E.g. home automation

- Distributed Controllers: These create a scalable network that share some intelligence but are essentially independent provide fault tolerance. E.g. locally networked gaming devices interact with an edge controller which can be failed over to another using centralized data in the cloud core

It is vitally important to recognize what isn’t Edge Computing. Most vendors are very eager to include all kinds of on premise deployments into the realm of Edge Computing. Here is a list of deployments that are NOT what they seem:

- On premise cloud deployments

- Pure play data forwarding platforms with only storage applications

- Single instance servers which don’t include any cloud elements like networking, clustered storage or fault tolerant computing cores

Who are the players in this market?

If you tell me that this is a trick question, then you will be right. Every single player who is not successful in the public cloud wars, are positioning themselves as champions of Edge Computing. This includes private cloud players (Vmware), hyperconverged appliance providers (Cisco), bare metal providers (SoftLayer), Storage networking vendors (NetApp), Database vendors (Oracle) and on premise server vendors (DELL). If you have noticed, all of them have hardware to sell!

This in turn has spurred their VARS to endlessly tout the promise of Edge Computing.

The reality is that the market for the wonderful technology that they have is slowly but surely slipping away because of the relentless promise of managed cloud services. Merchant silicon has taken over networking, commodity hardware is running storage, database as a service replaces core database applications and monitoring has virtually disappeared.

There is no reason to believe that the exact same thing will not happen at the edge since cost expectations are stringently lower.

Why is OpenStack perfect for Edge Computing?

Edge environments will initially be characterized by limited deployment room, constrained cloud uplink capabilities, uncertain power supply, lack of technical support expertise and very low cost footprints. Here is a cost outlay from a hyperconverged appliance vendor:

As for Cisco, how much will the HyperFlex System cost? According to CRN, the pricing for a three-node HX cluster starts at $60,000, including one year of 24x7x4 on-site support.

I fail to see how even a $10K appliance will be truly successful in true edge scenarios. There might be situations like Tele-ICUs that will invest this kind of money but it is not a sustainable business model. Edge Computing will commoditize the cloud contrary to heavy handed solutions dreamt up by enterprises hardware vendors.

In fact, Edge Computing may very well deploy software defined networking (SDN) to cobble together a viable economical solution using commodity hardware.

OpenStack on the other hand has no license baggage to be concerned about. It was built for commodity hardware and its overall capability can scale up/down depending on the quality of the hardware used. It is an open source platform and as noted earlier there are thousands of solution companies that have contributed code, expertise and direction. Hardware independence gives it the luxury of being able to drop off the technical support costs down a steep cliff.

Now this is a wedding I would like to see. Intel’s NUC appliance was featured for different workloads but when combined with a modular OpenStack, it can careen down the highway. The NUC is Xeon capable, embeds the i7 version of the chipset, accommodates 32GB of RAM and fits a 2.5 inch HDD/SSD. When you combine this with the power of a cloud stack then we have something cooking that will taste nice too!

There are serious advantages here:

- A low powered edge solution can be implemented that can scale to 1000s of nodes

- SDNs can be deployed to avoid expensive network hardware

- Inherently modular solution and easily replaceable

- Form factor will not be a deterrent and hence can be deployed in any location

- Any VAR can carry out hardware maintenance

- Extensive cooling is not necessary

And the tipping point would be

Like all good stories, the clincher would be a great solution recipe. Each edge scenario must be modelled into formulae that will clearly define hardware configuration, preselect software modules, preload applications and preordain authentication mechanisms. Recipes might be the best thing that happened to OpenStack given its perennial management/configuration problems.

OpenStack could really take a universal leap forward provided a few things go its way. It can draw consolation from the fact that almost every home router/set top box has some version of Linux running on it. It proves that standardization is vital to proliferation. An open sourced rack specification for mounting hardware would help immeasurably.

For 2020, the global smart home automation market is forecasted to reach 21 billion U.S. dollars. Smart homes totalled 30 million in 2016

If anyone told the OpenStack consortium that they could very well have 30 million potential landing spots, they should be thrilled to bits. This is just the proverbial tip of the iceberg as less than 0.001% of the houses in the world are smart homes. This does not include standard edge deployments and emerging multiplayer AR/VR gaming scenarios.

If you have ever seen this video by Corning, then you know that OpenStack would be wise to put down its marker right now.

IF the consortium can scale the stack down and simplify management, they could end up being a household name. Maybe then they call themselves The Edge!

I hope you enjoyed reading it and your comments are always welcome

Congratulations @adarshh! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on the badge to view your Board of Honor.

If you no longer want to receive notifications, reply to this comment with the word

STOPTo support your work, I also upvoted your post!

Downvoting a post can decrease pending rewards and make it less visible. Common reasons:

Submit